How Eastside Employees Are Converting Equity Into Property Wealth |

Strategic wealth diversification for the tech-savvy investor |

|

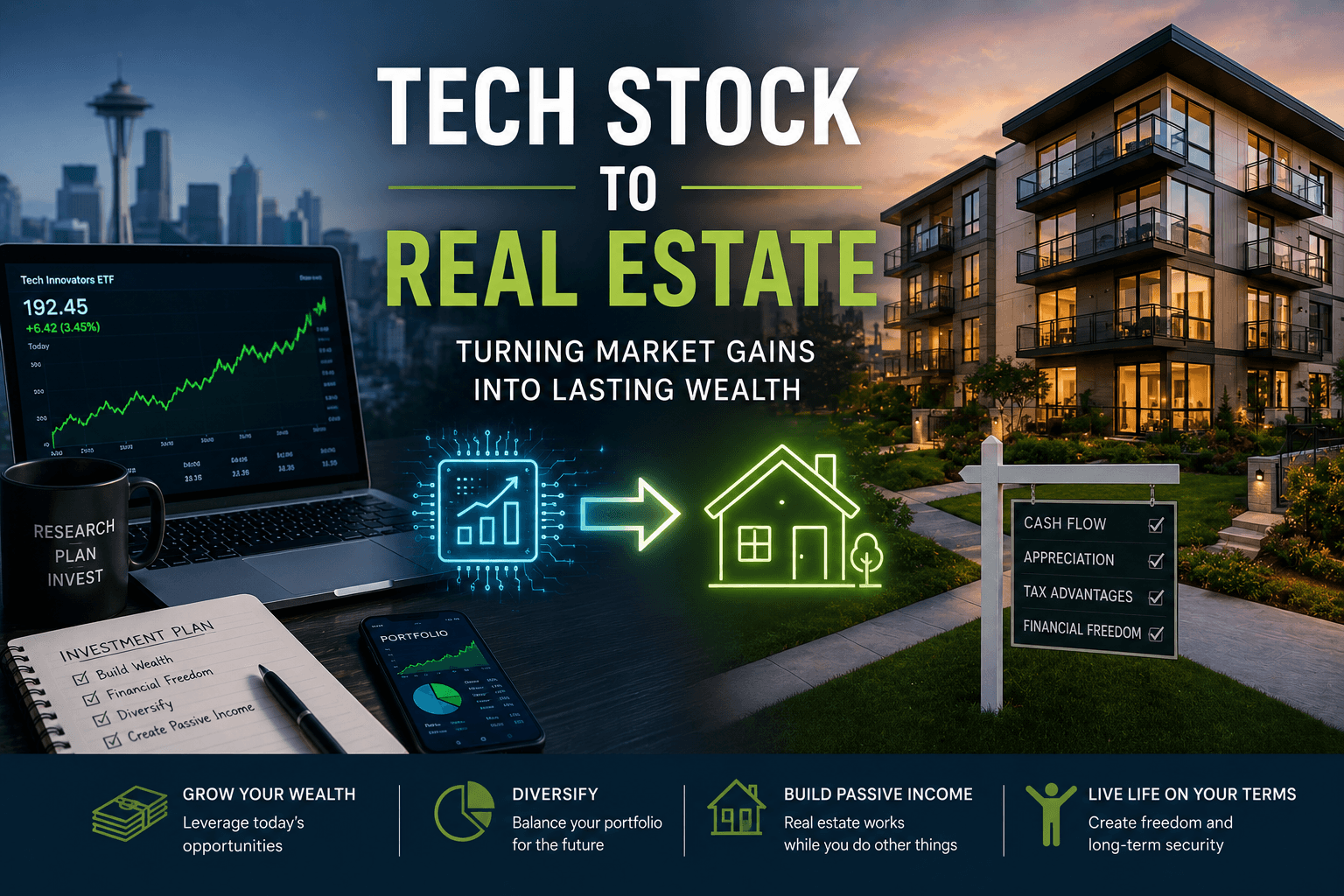

The Eastside tech corridor has created an unprecedented wealth generation machine. But here's what the employee handbook doesn't tell you: your RSUs are a time bomb of concentrated risk. The smartest employees I'm tracking aren't just watching their stock grants vest—they're executing systematic conversion strategies into hard assets.

The Equity TrapMicrosoft, Amazon, Meta—these companies have minted thousands of millionaires on paper. But paper wealth has an expiration date. I've watched colleagues ride their company stock from $200K to $2M and back down to $800K because they treated vesting schedules like gospel instead of exit signals.

Real wealth builders do something different: they diversify on a calendar, not on emotion. The 25% Rule in Action

Here's a framework that's working in Bellevue and Redmond right now: every vesting event, immediately convert 25% into real estate exposure. Not the entire amount into a single property—that's still concentration risk—but into diversified real estate instruments.

For a $100K vest after taxes (~$60K net), that's $15K into real estate. Do this quarterly, and you're building a parallel wealth engine that doesn't correlate with your employer's fortunes.

What That $15K Can Actually Buy

The Cascade EffectWhat makes this powerful isn't the individual moves—it's the compound diversification. After three years of systematic conversion, you're no longer a one-company portfolio. You've got tech equity, residential real estate, commercial exposure, and cash flow from rentals.

When your company stock dips 30% (and it will), you'll feel it. But you won't be devastated. That's the difference between paper millionaires and actual wealth.

Tax Optimization LayerThe sophisticated play here involves timing: harvest tax losses from underperforming positions to offset RSU income in high-vest years. Use 1031 exchanges when rolling appreciation from one property into larger deals. Structure rentals through LLCs that feed into your family wealth architecture.

This isn't just about buying real estate—it's about building a tax-efficient transfer system from equity compensation into generational assets. Execution Over Theory

The Eastside is full of people who know they should diversify. The difference-makers are the ones who automate it: vest → sell → allocate → deploy. No emotional decisions, no market timing, just systematic wealth transfer.

Your RSUs are a gift. Don't squander them on concentrated risk. Convert them into the kind of wealth that survives market cycles and pays your grandkids. |